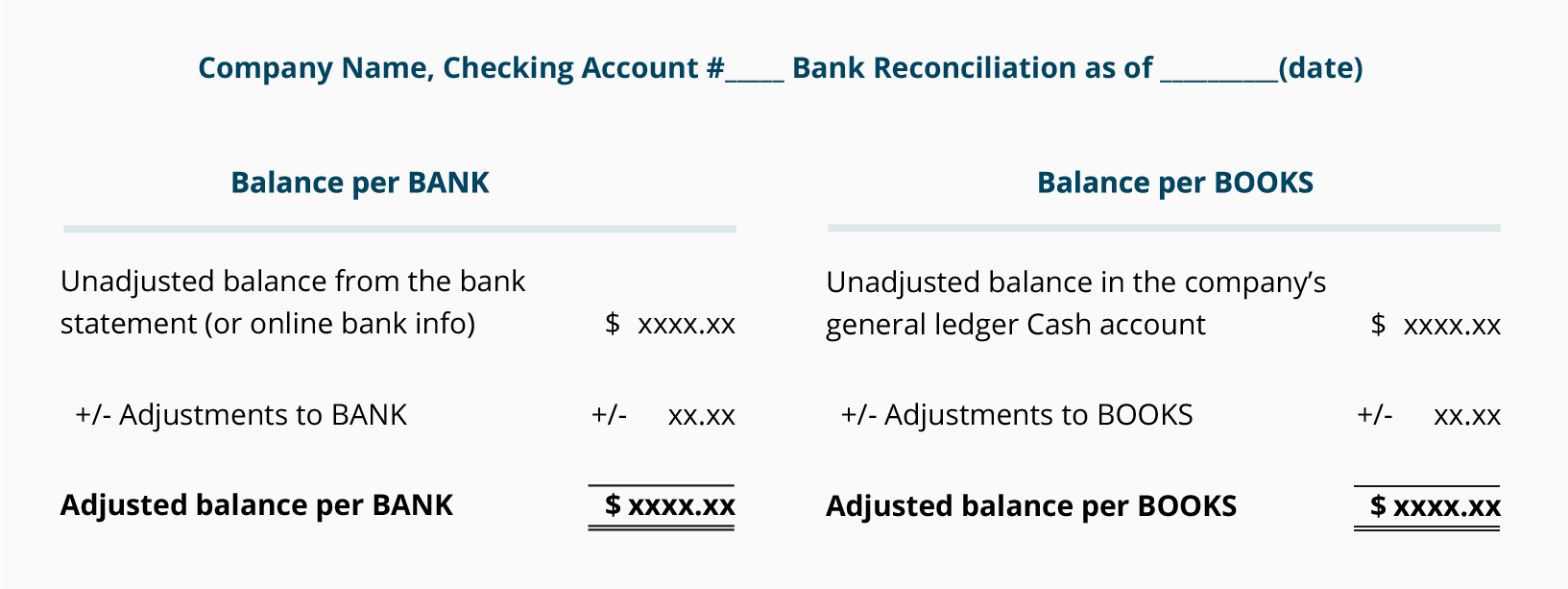

Introduction to Bank Reconciliation

A company's general ledger account Cash contains a record of the transactions (checks written, receipts from customers, etc.) that involve its checking account. The bank also creates a record of the company's checking account when it processes the company's checks, deposits, service charges, and other items. Soon after each month ends the bank usually mails a bank statement to the company. The bank statement lists the activity in the bank account during the recent month as well as the balance in the bank account.

Because most companies write hundreds of checks each month and make many deposits, reconciling the amounts on the company's books with the amounts on the bank statement can be time-consuming. The process is complicated because some items appear in the company's Cash account in one month, but appear on the bank statement in a different month. For example, checks written near the end of August are deducted immediately on the company's books, but those checks will likely clear the bank account in early September. Sometimes the bank decreases the company's bank account without informing the company of the amount. For example, a bank service charge might be deducted on the bank statement on August 31, but the company will not learn of the amount until the company receives the bank statement in early September. From these two examples, you can understand why there will likely be a difference in the balance on the bank statement vs. the balance in the Cash account on the company's books. It is also possible (perhaps likely) that neither balance is the true balance. Both balances may need adjustment in order to report the true amount of cash.

After you adjust the balance per bank to be the true balance and after you adjust the balance per books to also be the same true balance, you have reconciled the bank statement. Most accountants would simply say that you have done the bank reconciliation or the bank rec.

Bank Reconciliation Process

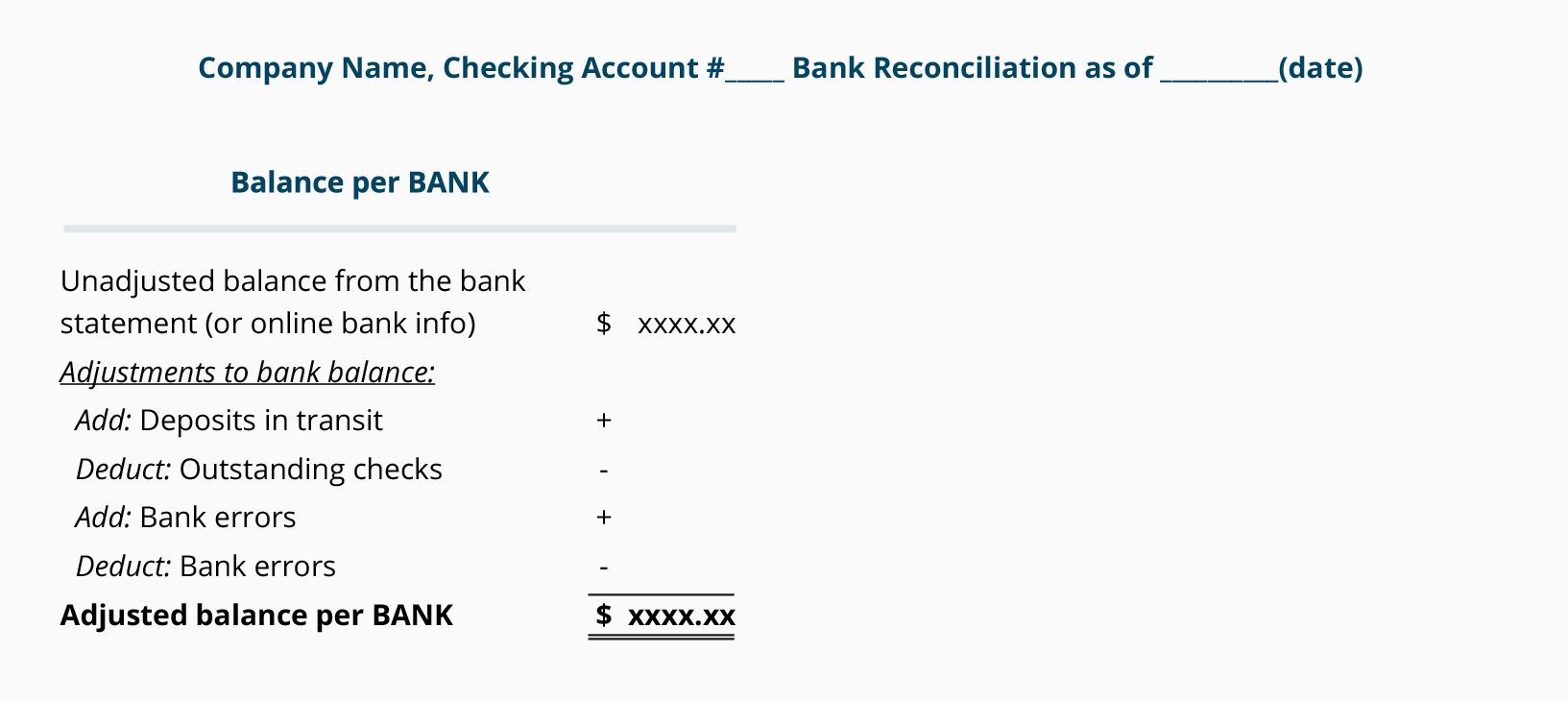

Step 1. Adjusting the Balance per Bank

We will demonstrate the bank reconciliation process in several steps. The first step is to adjust the balance on the bank statement to the true, adjusted, or corrected balance. The items necessary for this step are listed in the following schedule:

Deposits in transit are amounts already received and recorded by the company, but are not yet recorded by thebank. For example, a retail store deposits its cash receipts of August 31 into the bank's night depository at 10:00 p.m. on August 31. The bank will process this deposit on the morning of September 1. As of August 31 (the bank statement date) this is a deposit in transit.

Because deposits in transit are already included in the company's Cash account, there is no need to adjust the company's records. However, deposits in transit are not yet on the bank statement. Therefore, they need to be listed on the bank reconciliation as an increase to the balance per bank in order to report the true amount of cash.

- A helpful rule of thumb is "put it where it isn't." A deposit in transit is on the company's books, but it isn't on the bank statement. Put it where it isn't: as an adjustment to the balance on the bank statement.

Outstanding checks are checks that have been written and recorded in the company's Cash account, but have not yet cleared the bank account. Checks written during the last few days of the month plus a few older checks are likely to be among the outstanding checks.

Because all checks that have been written are immediately recorded in the company's Cash account, there is no need to adjust the company's records for the outstanding checks. However, the outstanding checks have not yet reached the bank and the bank statement. Therefore, outstanding checks are listed on the bank reconciliation as a decrease in the balance per bank.

- Recall the helpful tip "put it where it isn't." An outstanding check is on the company's books, but it isn't on the bank statement. Put it where it isn't: as an adjustment to the balance on the bank statement.

Bank errors are mistakes made by the bank. Bank errors could include the bank recording an incorrect amount, entering an amount that does not belong on a company's bank statement, or omitting an amount from a company's bank statement. The company should notify the bank of its errors. Depending on the error, the correction could increase or decrease the balance shown on the bank statement. (Since the company did not make the error, the company's records are not changed.)

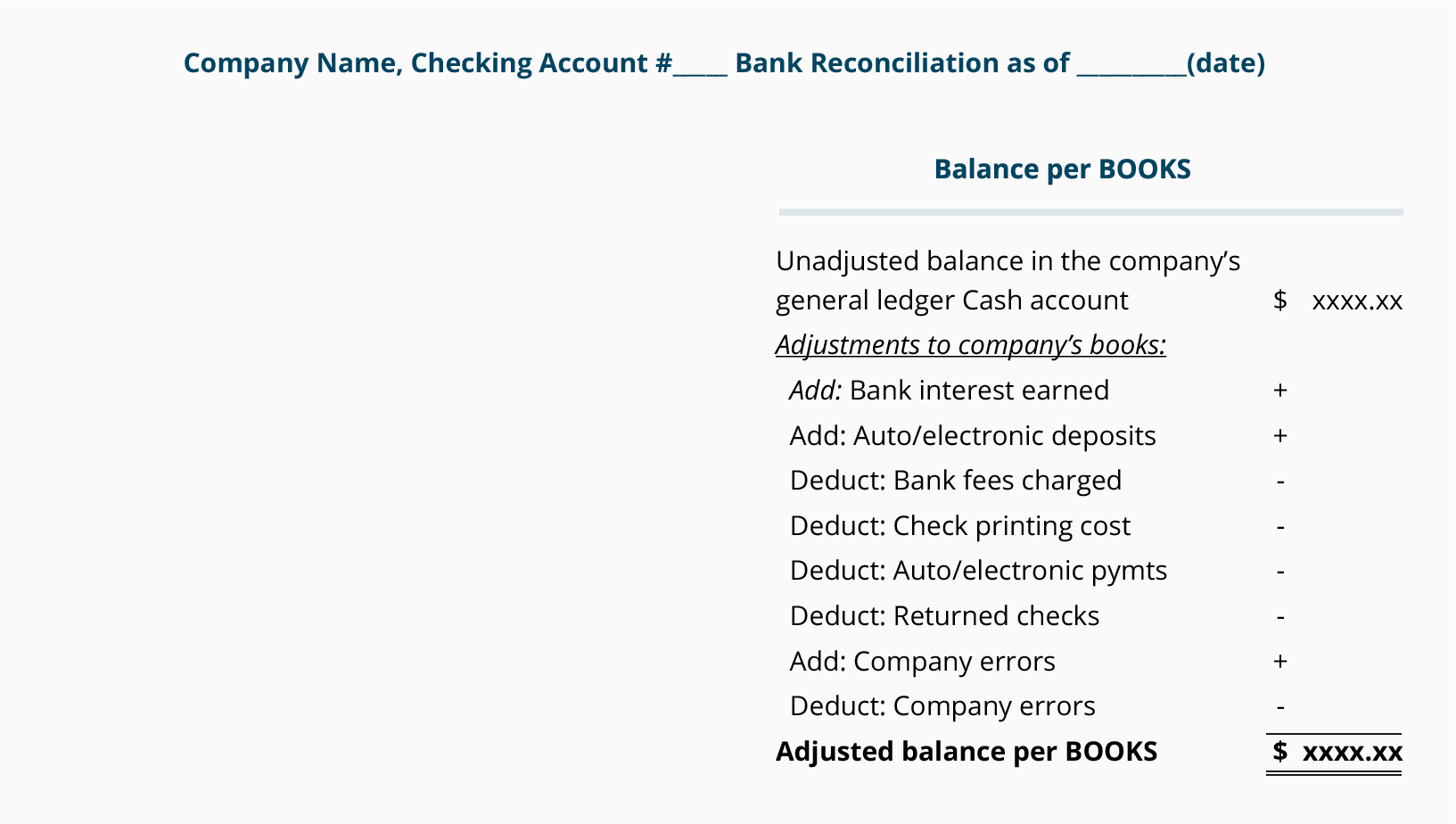

Step 2. Adjusting the Balance per Books

The second step of the bank reconciliation is to adjust the balance in the company's Cash account so that it is the true, adjusted, or corrected balance. Examples of the items involved are shown in the following schedule:

Bank service charges are fees deducted from the bank statement for the bank's processing of the checking account activity (accepting deposits, posting checks, mailing the bank statement, etc.) Other types of bank service charges include the fee charged when a company overdraws its checking account and the bank fee for processing a stop payment order on a company's check. The bank might deduct these charges or fees on the bank statement without notifying the company. When that occurs the company usually learns of the amounts only after receiving its bank statement.

Because the bank service charges have already been deducted on the bank statement, there is no adjustment to the balance per bank. However, the service charges will have to be entered as an adjustment to the company's books. The company's Cash account will need to be decreased by the amount of the service charges.

- Recall the helpful tip "put it where it isn't." A bank service charge is already listed on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

An NSF check is a check that was not honored by the bank of the person or company writing the check because that account did not have a sufficient balance. As a result, the check is returned without being honored or paid. (NSF is the acronym for not sufficient funds. Often the bank describes the returned check as a return item. Others refer to the NSF check as a "rubber check" because the check "bounced" back from the bank on which it was written.) When the NSF check comes back to the bank in which it was deposited, the bank will decrease the checking account of the company that had deposited the check. The amount charged will be the amount of the check plus a bank fee.

Because the NSF check and the related bank fee have already been deducted on the bank statement, there is no need to adjust the balance per the bank. However, if the company has not yet decreased its Cash account balance for the returned check and the bank fee, the company must decrease the balance per books in order to reconcile.

Check printing charges occur when a company arranges for its bank to handle the reordering of its checks. The cost of the printed checks will automatically be deducted from the company's checking account.

Because the check printing charges have already been deducted on the bank statement, there is no adjustment to the balance per bank. However, the check printing charges need to be an adjustment on the company's books. They will be a deduction to the company's Cash account.

- Recall the general rule, "put it where it isn't." A check printing charge is on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

Interest earned will appear on the bank statement when a bank gives a company interest on its account balances. The amount is added to the checking account balance and is automatically on the bank statement. Hence there is no need to adjust the balance per the bank statement. However, the amount of interest earned will increase the balance in the company's Cash account on its books.

- Recall "put it where it isn't." Interest received from the bank is on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

Notes Receivable are assets of a company. When notes come due, the company might ask its bank to collect the notes receivable. For this service the bank will charge a fee. The bank will increase the company's checking account for the amount it collected (principal and interest) and will decrease the account by the collection fee it charges.Since these amounts are already on the bank statement, the company must be certain that the amounts appear on the company's books in its Cash account.

- Recall the tip "put it where it isn't." The amounts collected by the bank and the bank's fees are on the bank statement, but they are not on the company's books. Put them where they aren't: as adjustments to the Cash account on the company's books.

Errors in the company's Cash account result from the company entering an incorrect amount, entering a transaction that does not belong in the account, or omitting a transaction that should be in the account. Since the company made these errors, the correction of the error will be either an increase or a decrease to the balance in the Cash account on the company's books.

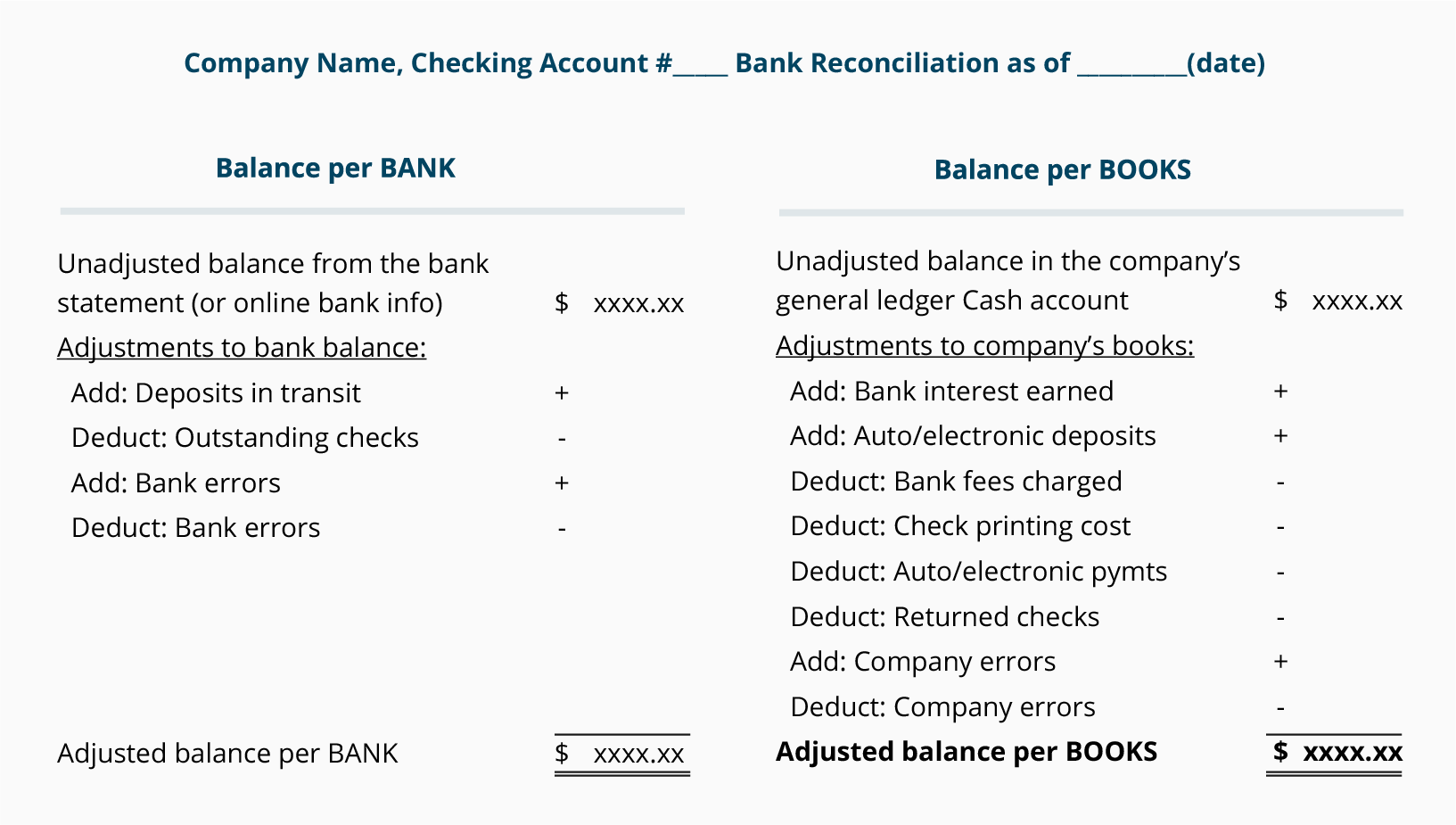

Step 3. Comparing the Adjusted Balances

After adjusting the balance per bank (Step 1) and after adjusting the balance per books (Step 2), the two adjusted amounts should be equal. If they are not equal, you must repeat the process until the balances are identical. The balances should be the true, correct amount of cash as of the date of the bank reconciliation.

Step 4. Preparing Journal Entries

Journal entries must be prepared for the adjustments to the balance per books (Step 2). Adjustments to increase the cash balance will require a journal entry that debits Cash and credits another account. Adjustments to decrease the cash balance will require a credit to Cash and a debit to another account.

Sample Bank Reconciliation with Amounts

In this part we will provide you with a sample bank reconciliation including the required journal entries. We will assume that a company has the following items:

| Item #1. |

The bank statement for August 2015 shows an ending balance of $3,490.

|

| Item #2. |

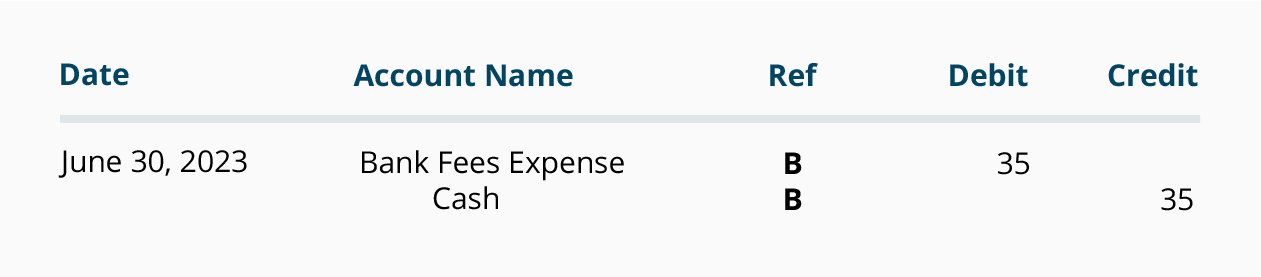

On August 31 the bank statement shows charges of $35 for the service charge for maintaining the checking account.

|

| Item #3. |

On August 28 the bank statement shows a return item of $100 plus a related bank fee of $10. The return item is a customer's check that was returned because of insufficient funds. The check was also marked "do not redeposit."

|

| Item #4. |

The bank statement shows a charge of $80 for check printing on August 20.

|

| Item #5. |

The bank statement shows that $8 was added to the checking account on August 31 for interest earned by the company during the month of August.

|

| Item #6. |

The bank statement shows that a note receivable of $1,000 was collected by the bank on August 29 and was deposited into the company's account. On the same day, the bank withdrew $40 from the company's account as a fee for collecting the note receivable.

|

| Item #7. |

The company's Cash account at the end of August shows a balance of $967.

|

| Item #8. |

During the month of August the company wrote checks totaling more than $50,000. As of August 31 $3,021 of the checks written in August had not yet cleared the bank and $200 of checks written in June had not yet cleared the bank.

|

| Item #9. |

The $1,450 of cash received by the company on August 31 was recorded on the company's books as of August 31. However, the $1,450 of cash receipts was deposited at the bank on the morning of September 1.

|

| Item #10. |

On August 29 the company's Cash account shows cash sales of $145. The bank statement shows the amount deposited was actually $154. The company reviewed the transactions and found that $154 was the correct amount.

|

Before we begin our sample bank reconciliation, learn the following bank reconciliation tip.

Here's a Tip

Put it where it isn't.

If an item appears on the bank statement but not on the company's books, the item is probably going to be an adjustment to the Cash balance on (per) the company's books.

If an item is already in the company's Cash account, but has not yet appeared on the bank statement, the item is probably an adjustment to the balance per the bank statement.

Our approach to the bank reconciliation is to prepare two schedules. The first schedule begins with the ending balance on the bank statement. We refer to this schedule as Step 1. The second schedule begins with the ending Cash account balance in the general ledger. We call this schedule Step 2.

Items 1 through 10 above have been sorted into the following schedules labeled Step 1 and Step 2. The item number is shown in the far right column of each schedule.

Step 1 Amounts

Let's review the schedule for Step 1. In all likelihood the balance shown on the bank statement is not the true balance to be reported on the company's balance sheet. The bank reconciliation process is to list the items that will adjust the bank statement balance to become the true cash balance. As the schedule for Step 1 indicates, the amount of deposits in transit must be added to the bank statement's balance. Also, the amount of checks that have been written, but not yet appearing on a bank statement, must be subtracted from the bank statement's balance. Next any bank errors should be listed and should be reported to the bank for correction. (The company does not report deposits in transit and/or outstanding checks to the bank.)

Step 2 Amounts and Required Journal Entries

Step 2 begins with the balance in the company's Cash account found in its general ledger. The bank reconciliation process includes listing the items that will adjust the Cash account balance to become the true cash balance. We will review each item appearing in Step 2 and the related journal entry that is required. Remember that any adjustment to the company's Cash account requires a journal entry. Generally, the adjustments to the books are the result of items found on the bank statement but have not yet been entered in the company's Cash account.

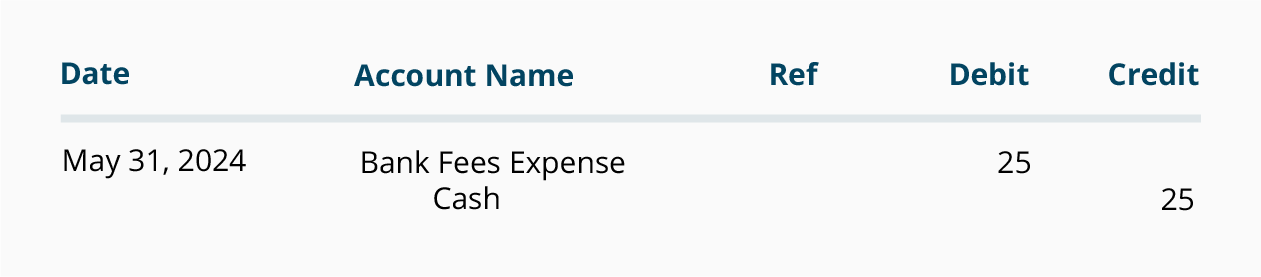

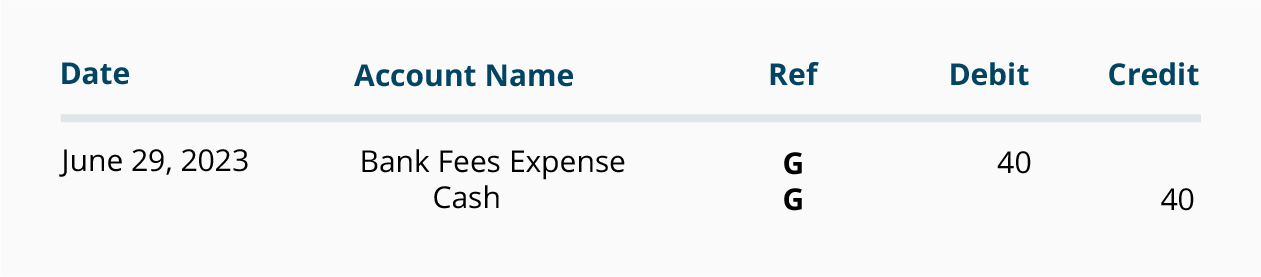

Item #2 Bank service charges. Since the bank deducted $35 from the company's checking account, but the company has not yet deducted this from its Cash account, the following journal entry needs to be made.

(If the annual amount of service charges is small, debit Miscellaneous Expense.)

Item #3 NSF checks and fees. Since the bank deducted these legitimate amounts from the company's bank account, the company will need to deduct these amounts from its Cash account. As mentioned, the NSF check of $100 was from a customer. Therefore, the company will likely undo the reduction to Accounts Receivable that took place when the company originally processed the $100 check. If the company wishes to recover the bank fee of $10 from the customer, it should add the $10 fee to the amount that the customer owes the company. The journal entry might look like this:

(If the amount cannot be recovered from the customer, charge an expense.)

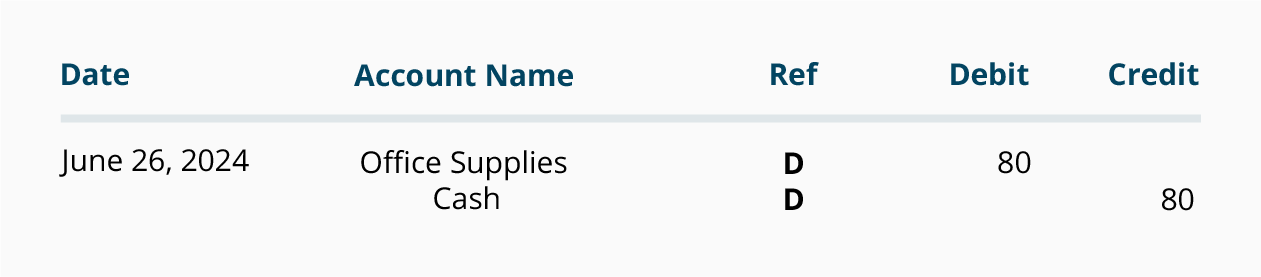

Item #4 Check printing charges. Because this expense is not yet entered on the company's books, but the amount has been deducted from its bank account, the company will make the following journal entry.

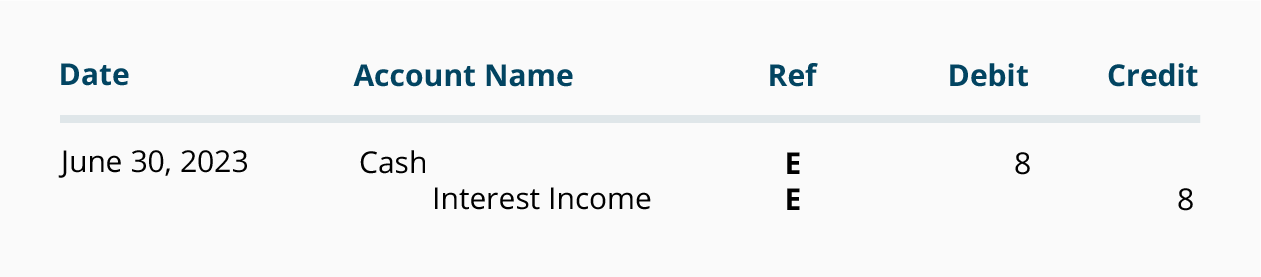

Item #5 Interest earned. The bank increased the checking account balance by $8 on August 31. Since the bank did not notify the company previously, the company must now increase the balance in its Cash account.

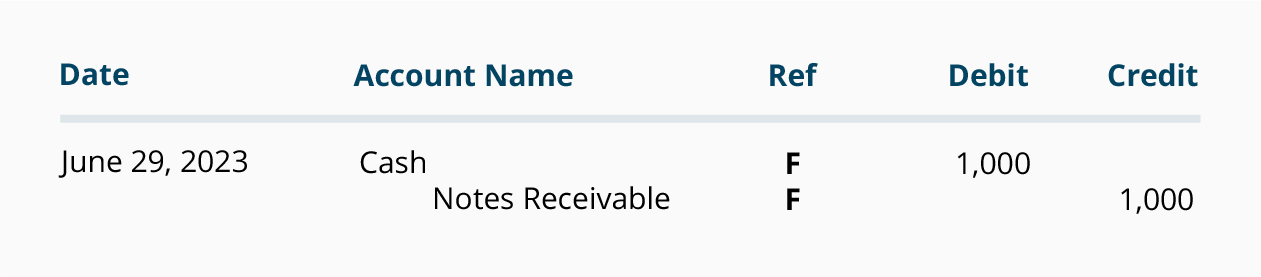

Item #6 Notes receivable collected. The bank increased the company's checking account when it collected a note for the company on August 29. It was determined that the company had not yet made an entry to its Cash account for this transaction. As a result the following journal entry is needed.

Item #10 Company error. The company had entered $145 in its Cash account on August 29, but the bank statement showed the correct amount: $154. The transaction involved the cash sales for the day. As a result the company's Cash account will have to be increased by $9 as follows:

Step 3 Comparing the Adjusted Balances

In the above schedules the adjusted balance for Step 1 is $1,719 and the adjusted balance for Step 2 is $1,719. The company believes that all items involving cash have been included in the schedules. As a result the company has successfully completed its bank reconciliation as of the August 31, 2015.

Additional Information and Resources

Because the material covered here is considered an introduction to this topic, many complexities have been omitted. You should always consult with an accounting professional for assistance with your own specific circumstances.

Good Post!

ReplyDeleteThanks for sharing this information about Bank Reconciliation.

Bank Reconciliation UK

I want to learn

ReplyDelete